4QFY2018 Result Update | Media

May 28, 2018

LT Foods

BUY

CMP

`76

Performance Update

Target Price

`128

(` cr)

4QFY18

4QFY17

% yoy

3QFY18

% qoq

Investment Period

12 Months

Revenue

1,071

927

15.4

941

13.8

Sector

Food Processing

EBITDA

96

93

3.7

86

12.0

Market Cap (` cr)

2,454

Net Debt (` cr)

1,516

OPM (%)

9.0

10.0

(102)

9.1

(14)

Beta

1.0

A djusted PAT

35

38

(8.8)

39

(10.3)

52 Week High / Low

109/56

Avg. Daily Volume

30,429

Source: Company, Angel Research

Face Value (`)

1

BSE Sensex

35,134

For 4QFY2018, LT Foods Ltd (LTFL) posted results in-line with our expectations on

Nifty

10,675

Reuters Code

LTOL.BO

the top-line front. However it disappointed on the bottom-line front. Revenue grew

Bloomberg Code

LTFO.IN

by ~15% yoy to `1,071cr, driven by healthy growth in domestic as well as

Shareholding Pattern (%)

international businesses. On the operating front, margins contracted by 102bps

Promoters

56.0

MF / Banks / Indian Fls

17.7

yoy on account of investment on expansion of international operations in Europe

FII / NRIs / OCBs

0.0

& US and currency fluctuation. On the bottom-line front, PAT de-grew by ~8%

Indian Public / Others

26.3

ypy to `35cr on account of poor operating margin and higher depreciation cost.

Abs.(%)

3m 1yr

3yr

Sensex

7.4

27.1

22.9

Healthy revenue growth in domestic and international businesses aided top-line:

LT Foods

(19.2)

2.7

442.0

The company’s top-line grew by ~15% yoy to `1,071cr on the back of strong

domestic growth (up by ~9%) and international growth (up by ~31%). During

FY18, share of branded revenues to overall revenues has increased from 64% to

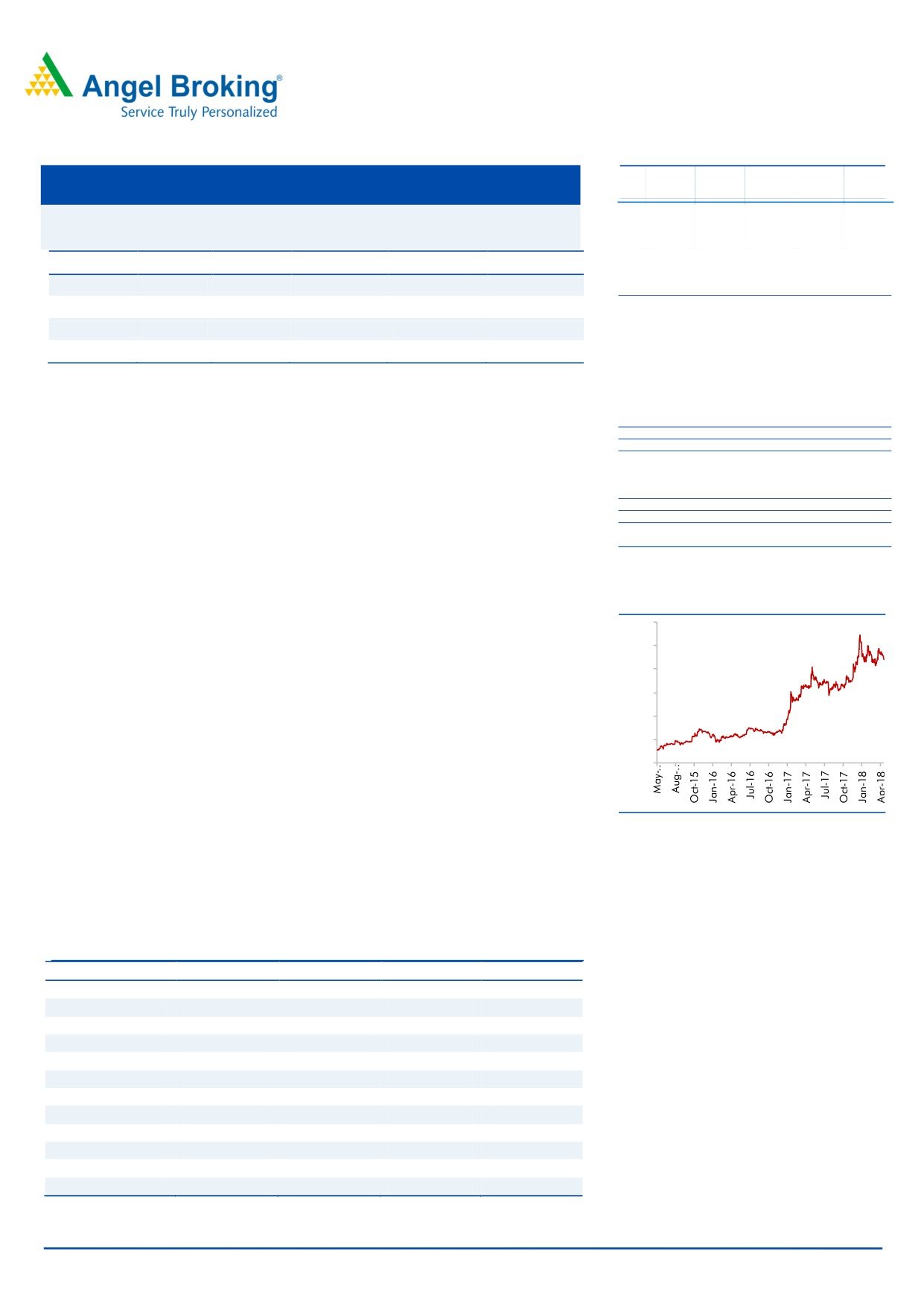

3-year price chart

69%. Moreover during FY18, LTFL has launched the new avatar of leading brand

120

“Daawat” and quick cook brown rice. These new initiatives are expected to give a

new look and feel to the brand, along with more information to the consumer.

100

Profitabilty tepid due to poor operating margins and higher depreciation cost: On

80

the operating front, margins contracted by 100bps yoy on account of investment

60

on expansion of international operations in Europe & US and currency fluctuation.

40

On the bottom-line front, PAT de-grew by ~8% to `35cr on an account of poor

20

operating margin and higher depreciation cost.

-

Outlook and Valuation: Going forward, we expect the company to report healthy

top-line CAGR of 12% over the next two years on the back of strong distribution

network & brand, continuing expansion, wide product basket and addition of new

Source: Company, Angel Research

products in portfolio. On the bottom-line front, we expect ~17% CAGR following

robust improvement in operating performance over the next two years. We expect

margin expansion from better manufacturing efficiency, increase in scale and

change in product mix. At the current market price of `76, the stock trades at a PE

of 15.8x and 12.6x its FY2019E and FY2020E EPS of `4.9 and `6.1 respectively.

We recommend BUY with target price of `128.

Key financials

Amarjeet S Maurya

Y/E March (`cr)

FY2017

FY2018

FY2019E

FY2020E

022-39357800 Ext: 6831

Net Sales

3,287

3,614

4,047

4,533

% chg

10.5

10.0

12.0

12.0

Net Profit

117

144

156

196

% chg

18.9

23.0

8.0

25.8

OPM (%)

11.1

10.4

10.8

11.0

EPS (`)

3.7

4.5

4.9

6.1

P/E (x)

21.0

17.1

15.8

12.6

P/BV (x)

3.8

2.1

1.8

1.6

RoE (%)

17.9

12.0

11.5

12.6

RoCE (%)

13.8

12.0

12.7

13.7

EV/Sales (x)

1.2

1.1

1.0

0.9

EV/EBITDA (x)

11.0

10.5

9.1

8.0

Source: Company, Angel Research, Note: CMP as of May 28, 2018

Please refer to important disclosures at the end of this report

1

LT Foods | 4QFY2018 Result Update

Exhibit 1: 4QFY2018 Performance

Y/E March (` cr)

4QFY18

4QFY17

% yoy

3QFY18

% qoq

FY2018

FY2017

% chg

Net Sales

1,071

927

15.4

941

13.8

3613.7

3244.8

11.4

Consumption of RM

829.9

725.45

14.4

713.8

16.3

2671.4

2409.7

10.9

(% of Sales)

77.5

78.2

75.9

73.9

74.3

Staff Costs

39

35

10.2

34

13.6

135.0

116.9

15.5

(% of Sales)

3.6

3.8

3.6

3.7

3.6

Other Expenses

106

74

42.9

107

(1.1)

431.0

360.2

19.6

(% of Sales)

9.9

8.0

11.4

11.9

11.1

Total Expenditure

975

835

16.7

855

14.0

3,237

2,887

12.1

Operating Profit

96

93

3.7

86

12.0

376

358

5.1

OPM

9.0

10.0

9.1

10.4

11.0

Interest

40

39

2.6

33

20.4

146.6

156.8

(6.5)

Depreciation

18

13

33.7

12

52.2

50.1

55.1

(9.0)

Other Income

8

17

18

36.2

48.1

PBT (excl. Ext Items)

46

58

(20.4)

58

(21.2)

216

194

11.1

Ext (Income)/Expense

PBT (incl. Ext Ite ms)

46

58

(20.4)

58

(21.2)

216

194

11.1

(% of Sales)

4.3

6.2

6.2

6.0

6.0

Provision for Taxation

11

20

20

71.4

64.9

10.0

(% of PBT)

24.8

34.4

33.9

33

33

Reported PAT

35

38

(8.8)

39

(10.3)

144

129

11.7

PATM

3.2

4.1

4.1

4.0

4.0

Minority Interest After NP

Extra-ordinary Items

Reported PAT

34.57

37.89

(8.8)

38.56

(10.3)

144.42

129.27

11.7

Equity shares (cr)

36

36

36

36

36

FDEPS (`)

1.0

1.0

(8.8)

1.1

(10.3)

4.0

3.6

11.7

Source: Company, Angel Research

May 28, 2018

2

LT Foods | 4QFY2018 Result Update

Key investment arguments

Market leadership with strong brand visibility:

LTFL’s flagship brand Daawat enjoys 22% market share in the branded rice market

in India. The company has strong market share in North America selling Basmati

rice under the brand name ‘Royal’. Historically, the company has been focusing on

strong brand visibility, and in order to enhance brand visibility it has significant ad

spend.

Wide distribution network

Currently, LTFL has access to 1,40,000 traditional retail outlets, covering 93% of

towns with over 2 lakh population and 3,000 wholesalers. Further, the company

sells its products to premium hotels & restaurants (~50% share), and has access to

6,000 foodservice outlets i.e. ‘DawatChefs Secretz”. Moreover, it has access to

2,500 modern trade stores including 121 hypermarkets, 298 supermarkets and

1,462 mini markets. It is also the first Rice Company to place Brown Basmati Rice

in Medical Chains.

Diversified product portfolio catering to varied customers

LTFL has a well-diversified product basket, which caters to consumers of all income

groups. The company is present in segments like Basmati rice, Speciality rice (non-

Basmati) and other food products. It is also consistently working on adding new

products to its portfolio. LTFL has done JV with Japanese Snack Food major

Kameda, which would launch rice based snacks in India. LTFL has recently

introduced ‘Daawat Rozana GoldPlus’ brand.

Strong global footprint

LT Foods is now an emerging global Foods Company with focus on basmati and

other speciality rice, organic foods and convenience rice-based products. LT Foods

has a global footprint, selling their flagship basmati rice brands Royal and Daawat

into 65 countries. The company has established on ground presence in the US,

Europe and Middle East in order to unlock the full potential of these territories.

May 28, 2018

3

LT Foods | 4QFY2018 Result Update

Outlook and Valuation

Going forward, we expect the company to report healthy top-line CAGR of 12%

over the next two years on the back of strong distribution network & brand,

continuing expansion, wide product basket and addition of new products in

portfolio. On the bottom-line front, we expect ~17% CAGR following robust

improvement in operating performance over the next two years. We expect margin

expansion from better manufacturing efficiency, increase in scale and change in

product mix. At the current market price of `76, the stock trades at a PE of 15.8x

and 12.6x its FY2019E and FY2020E EPS of `4.9 and `6.1 respectively. We

recommend BUY with target price of `128.

Risks

Increase in competition from unorganized players would impact overall

growth prospects of the company.

Basmati rice is an extremely volatile commodity. Hence, any unfavorable

change in Basmati rice prices could impact the company’s profitability.

Company derives ~52% revenue from overseas market; any unfavorable

change in currency could have an adverse impact on the company’s

profitability.

Company Background

LT Foods Limited (LTFL) is a branded speciality foods company engaged in milling,

processing and marketing of branded and non-branded basmati rice, and

manufacturing of rice food products in the domestic and overseas markets. Its

geographical segments include India, North America and Rest of the World. The

major brands of the company are Daawat, Gold Seal Indus Valley, Rozana and

817 Elephant.

May 28, 2018

4

LT Foods | 4QFY2018 Result Update

Consolidated Profit & Loss Statement

Y/E March (`cr)

FY2017

FY2018

FY2019E

FY2020E

Total operating income

3,287

3,614

4,047

4,533

% chg

10.5

10.0

12.0

12.0

Total Expenditure

2,920

3,237

3,610

4,034

Raw Material

2,405

2,671

2,975

3,318

Personnel

117

135

154

177

Others Expenses

398

431

482

539

EBITDA

366

376

437

499

% chg

17.2

2.7

16.2

14.1

(% of Net Sales)

11.1

10.4

10.8

11.0

Depreciation& Amortisation

54

50

71

74

EBIT

312

326

366

425

% chg

19.5

4.5

12.3

16.1

(% of Net Sales)

9.5

9.0

9.0

9.4

Interest & other Charges

155

147

143

142

Other Income

36

36

10

10

(% of PBT)

18.4

16.8

4.3

3.4

Share in profit of Associ ates

-

-

-

-

Recurring PBT

193

216

233

293

% chg

61.5

11.8

7.9

25.8

Tax

64

71

77

97

(% of PBT)

33.3

33.1

33.0

33.0

PAT (reported)

129

144

156

196

Minority Interest (after tax)

10

-

-

-

Profit/Loss of Associate Company

(1)

-

-

-

Extraordinary Items

-

-

-

-

ADJ. PAT

117

144

156

196

% chg

18.9

23.0

8.0

25.8

(% of Net Sales)

3.6

4.0

3.9

4.3

Basic EPS (`)

3.7

4.5

4.9

6.1

Fully Diluted EPS (`)

3.7

4.5

4.9

6.1

% chg

18.9

23.0

8.0

25.8

May 28, 2018

5

LT Foods | 4QFY2018 Result Update

Exhibit 2: Consolidated Balance Sheet

Y/E March (` cr)

FY2017

FY2018

FY2019E

FY2020E

SOURCES OF FUNDS

Equity Share Capital

27

32

32

32

Reserves& Surplus

630

1,169

1,325

1,521

Shareholders Funds

656

1,201

1,357

1,553

Minority Interest

45

45

45

46

Total Loans

1,612

1,516

1,536

1,556

Deferred Tax Liability

5

5

5

6

Total Liabilities

2,318

2,767

2,943

3,161

APPLICATION OF FUNDS

Gross Block

736

926

966

996

Less: Acc. De preciation

365

416

487

560

Net Block

371

510

479

436

Capital Work-in-Progress

40

40

40

40

Investments

5

5

5

5

Current Assets

2,299

2,630

2,865

3,186

Inventories

1,448

1,729

1,941

2,173

Sundry De btors

463

495

554

621

Cash

41

29

34

43

Loans & Advances

179

215

174

168

Other Assets

167

163

162

181

Current liabilities

410

445

489

565

Net Current Assets

1,889

2,186

2,376

2,621

Deferred Tax Asset

13

13

13

14

Mis. Exp. not written off

-

-

-

-

Total Assets

2,318

2,754

2,914

3,116

Source: Company, Angel Research

May 28, 2018

6

LT Foods | 4QFY2018 Result Update

Exhibit 3: Consolidated Cashflow Statement

Y/E March (`cr)

FY2017

FY2018

FY2019E FY2020E

Profit before tax

195

216

233

293

Depreciation

54

50

71

74

Change in Working Capital

(125)

(308)

(186)

(236)

Interest / Dividend (Net)

143

147

143

142

Direct taxes paid

(44)

(71)

(77)

(97)

Others

(7)

0

0

0

C ash Flow from Operati ons

217

33

185

176

(Inc.)/ Dec. i n Fixed Assets

(85)

(220)

(40)

(30)

(Inc.)/ Dec. i n Inve stments

(4)

0

0

0

C ash Flow from Inve sting

(89)

(220)

(40)

(30)

Issue of Equity

2

0

0

0

Inc./(Dec.) in loans

23

(95)

20

20

Dividend Paid (Incl. T ax)

(4)

0

0

0

Interest / Divide nd (Net)

(145)

282

(159)

(157)

C ash Flow from Financing

(124)

186

(139)

(137)

Inc./(Dec.) in Cash

4

(1)

5

9

O pening Cash balance s

26

30

29

34

Closing Cash balances

30

29

34

43

Source: Company, Angel Research

May 28, 2018

7

LT Foods | 4QFY2018 Result Update

Key Ratios

Y/E March

FY2017

FY2018

FY2019E

FY2020E

Valuati on Ratio (x)

P/E (on FDEPS)

21.0

17.1

15.8

12.6

P/CEPS

13.5

12.7

10.9

9.1

P/BV

3.8

2.1

1.8

1.6

Dividend yield (%)

0.0

0.0

0.0

0.0

EV/Sales

1.2

1.1

1.0

0.9

EV/EBITDA

11.0

10.5

9.1

8.0

EV / Total Assets

1.7

1.4

1.4

1.3

Per Share Data (`)

EPS (Basic)

3.7

4.5

4.9

6.1

EPS (fully diluted)

3.7

4.5

4.9

6.1

Cash EPS

5.7

6.1

7.1

8.4

DPS

0.0

0.0

0.0

0.0

Book Value

20.5

37.5

42.4

48.6

Returns (%)

ROCE

13.8

12.0

12.7

13.7

Angel ROIC (Pre-tax)

14.0

12.2

12.8

13.9

ROE

17.9

12.0

11.5

12.6

Turnover rati os (x)

Asset Turnover (Gross Block)

4.5

3.9

4.2

4.6

Inventory / Sales (days)

161

175

175

175

Receivables (days)

51

50

50

50

Payable s (days)

24

24

24

25

Working capital cycle (ex-cash) (days)

188

201

201

200

May 28, 2018

8

LT Foods | 4QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration numb er

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/ben eficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as th e basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document sho uld

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to de termine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in th is report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that ma y arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please r efer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

LT Foods

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

MaNote: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

9

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)